The Statutory Residence Test (SRT) looks deceptively simple on paper. Three automatic tests, a days-based calculation, and a handful of "ties" to the UK, what could go wrong? Quite a lot, actually.

HMRC reviews thousands of residence determinations each year, and the mistakes they find can cost taxpayers tens of thousands of pounds in unexpected tax bills, interest, and penalties. The self-assessment system places the burden entirely on you to get it right, and "I didn't know" isn't a defence that holds much water.

If you're moving abroad, returning to the UK, or spending time in multiple countries, here are seven costly mistakes you absolutely need to avoid when applying the statutory residence test in 2026.

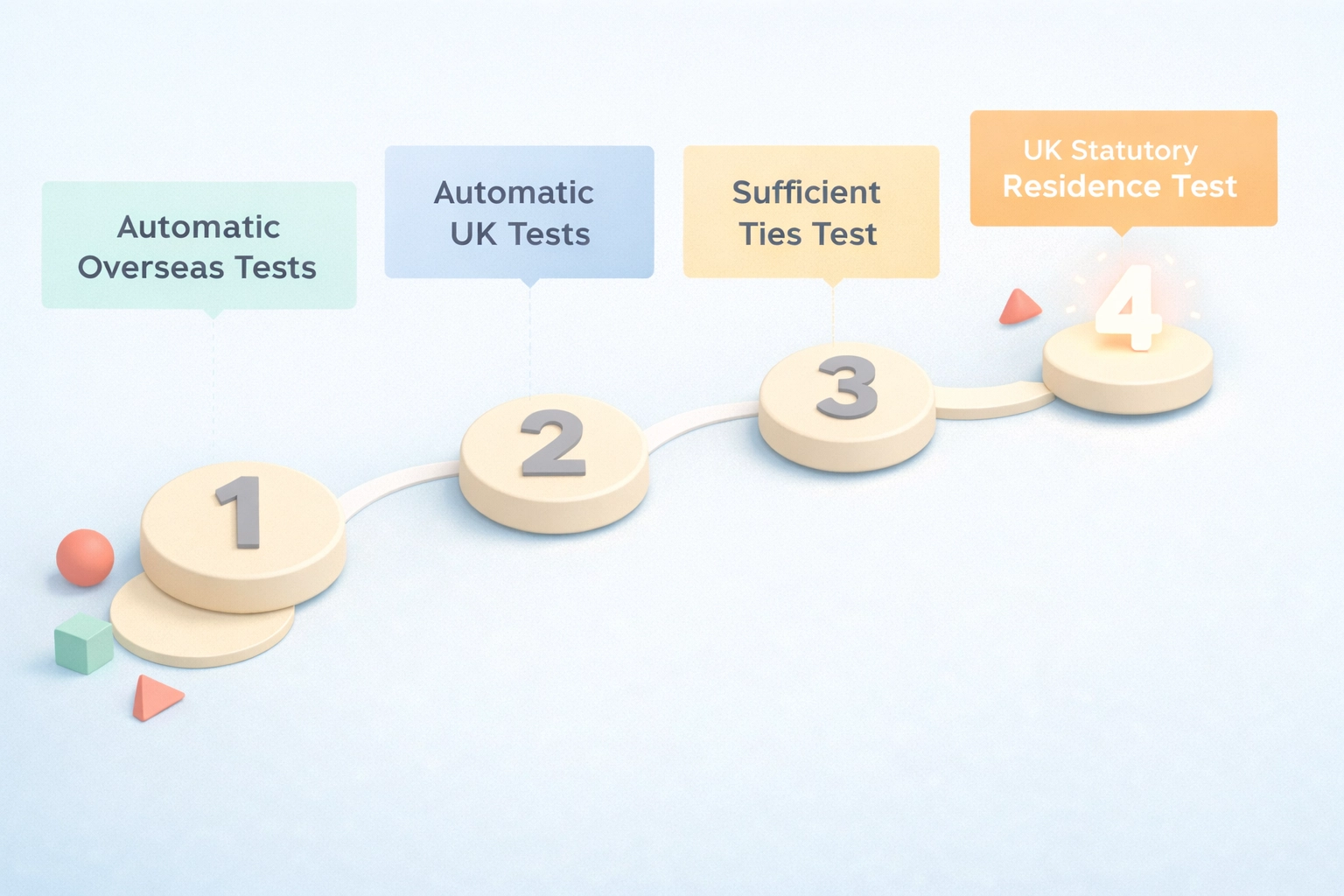

Mistake #1: Applying the SRT Tests in the Wrong Order

Here's the thing most people miss: the statutory residence test isn't a buffet where you pick the rule that suits you best. It's a strict sequential process, and you must apply the tests in this exact order:

The 183-day automatic UK residence test

The automatic overseas tests (which prove non-residence)

The automatic UK residence tests

The sufficient ties test (only if none of the above apply)

You cannot skip ahead to the sufficient ties test just because it gives you a better outcome. If you meet the 183-day test (spending 183 days or more in the UK during the tax year), you're automatically UK resident, end of story. No ties analysis needed.

Similarly, if you meet one of the automatic overseas tests, you're automatically non-resident, regardless of how many UK ties you might have.

The sequential application catches out a surprising number of taxpayers who attempt to cherry-pick the most favourable test. Don't be one of them.

Mistake #2: The "Only Home" Trap

This one stings, and it catches nearly everyone who's in the process of relocating abroad. The automatic UK residence test includes a provision for those who have a home in the UK. Specifically, you're automatically UK resident if:

You have only one home during the tax year, and that home is in the UK

You spend at least 30 days in that UK home during the year

There's a 91-day period when you either have no overseas home or spend fewer than 30 days using an overseas home

The trap? Even if you've already decided to move abroad and are actively house-hunting overseas, you can still trigger UK residence if you haven't yet secured that foreign property.

Let's say you put your UK home on the market in April but don't complete on your Spanish villa until July. During that 91-day window, you've only got the UK home. If you've spent 30+ days there during the tax year, you've just become automatically UK resident, regardless of your intentions or where you spend the rest of the year.

The lesson: timing matters enormously when you're relocating. Overlap your properties if possible, or ensure you have documentary evidence of a settled overseas home (rental agreements, purchase contracts) before you increase your UK presence.

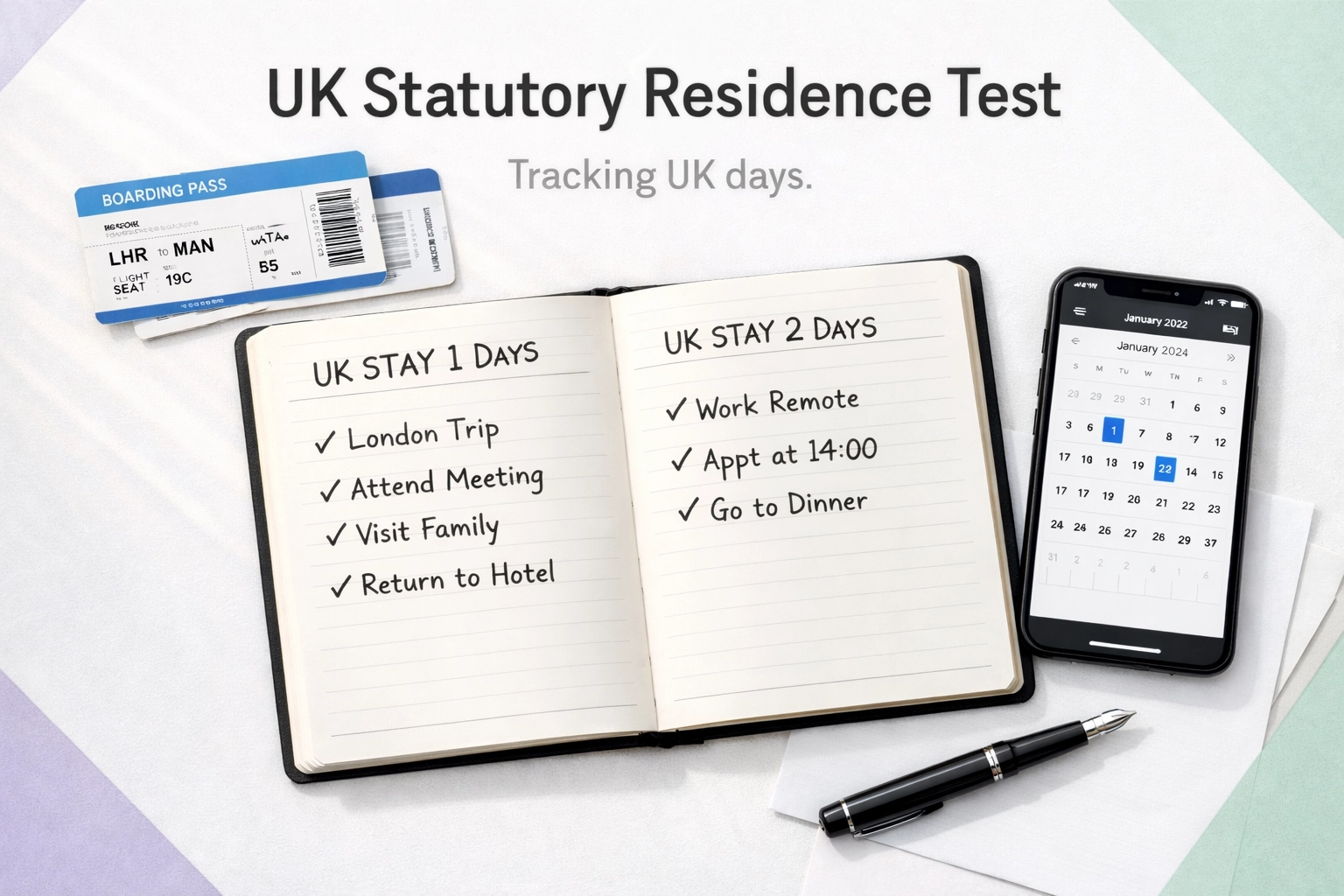

Mistake #3: Sloppy Day-Count Tracking

This sounds basic, but it's the single most common error we see at Global Tax Consulting. For the statutory residence test, every midnight you spend in the UK counts as a UK day. That includes:

Transit days (yes, even if you're just passing through Heathrow)

Days when you arrive late at night or leave early in the morning

Days when you're working remotely from a UK location

Days spent in UK territorial waters on ships or oil rigs

The only days you can exclude are those where exceptional circumstances prevent you from leaving the UK (think serious illness requiring emergency medical treatment, or natural disasters). And even then, you need contemporaneous documentation proving you genuinely couldn't arrange alternatives.

HMRC has access to your border crossing data, passport stamps, employment records, and financial transaction locations. If you've casually rounded down your UK days or "forgotten" a few long weekends, you're creating compliance risk that can come back to haunt you years later.

Keep meticulous records: flight confirmations, hotel bookings, credit card statements showing where you were. A simple spreadsheet tracking every entry and exit saves enormous hassle down the line.

Mistake #4: Misunderstanding What Counts as a "Home"

The word "home" has a specific meaning in the statutory residence test, and it's not the same as "property I own." A home requires a degree of permanence, stability, and use. HMRC's guidance suggests it should be available for your use for at least 91 consecutive days and be used as a genuine residence, not just an investment property or occasional holiday let. This creates grey areas that trip people up:

Does your UK buy-to-let count as a home? Generally no, if it's tenanted and you're not using it for personal accommodation. But if you retain access or use it between tenants, it might.

What about your Airbnb in Portugal that you visit twice a year? Probably not a home: it lacks the permanence and regular use required.

Does staying with family count? Potentially, if you have a dedicated space and regular, ongoing access.

The definition becomes especially murky when you own multiple UK properties or have holiday homes abroad. Each case turns on its specific facts, and assuming you know how HMRC will interpret "home" without professional input is risky.

Mistake #5: Ignoring or Misunderstanding UK "Ties"

If you don't meet any of the automatic tests, the sufficient ties test determines your residence status by combining your UK day count with your number of UK ties.

The ties are:

Family tie: spouse, civil partner, or minor children resident in the UK

Accommodation tie: available UK accommodation used during the year

Work tie: working in the UK for 40+ days (at least 3 hours per day)

90-day tie: spending more than 90 days in the UK in either of the previous two tax years

Country tie: spending more days in the UK than any other single country (only for leavers)

Each tie you have reduces the number of days you can spend in the UK before becoming resident. For example, if you were UK resident in one of the previous three years and have three ties, you can only spend 45 days in the UK before triggering residence. With four ties, that drops to just 15 days.

The mistakes people make:

Not realising that adult children count if they're under 18 at any point during the tax year

Assuming accommodation doesn't count if they're not the legal owner (it does: "available for use" is the test)

Miscounting work days by excluding short meetings or conference calls

Forgetting that the 90-day tie looks backwards at the previous two years

You need to calculate your ties meticulously and understand how they interact with your day count. It's not just about staying under 183 days: your ties might mean you need to stay under 45 days, or even 15.

Split-year treatment can be a lifesaver if you're leaving or arriving in the UK mid-year, but the timing isn't what most people assume.

If you qualify for split-year treatment, the tax year is divided into a UK-resident part and a non-UK-resident part. You only pay UK tax on your worldwide income during the UK-resident portion.

The mistake: assuming the split happens on your departure or arrival date. It doesn't. For overseas employment cases (the most common scenario for leavers), the UK-resident part of the year ends on the day before you start full-time work overseas. If you've planned a two-week settling-in period before starting your new Dubai job, those two weeks still fall into your UK-resident period.

That means any income, gains, or distributions you receive during your "transition period" could still be fully taxable in the UK, even though you've physically left and consider yourself an expat. Similarly, for arrivals, the non-UK-resident part doesn't necessarily end when you land at Heathrow. The start date depends on which split-year case applies to you, and each has different criteria.

The lesson: don't assume. Check the specific split-year case that applies to your circumstances and plan the timing of any significant income events accordingly.

Mistake #7: Relying on DIY Tax Planning

The statutory residence test might look straightforward in flowchart form, and there's no shortage of online calculators promising to tell you whether you're UK resident. But here's the reality: the SRT is fiendishly complex when applied to real-world situations. The automatic tests contain multiple conditions that must all be met. The ties test requires detailed analysis of your last three years. The definitions of "home," "accommodation," and "work" are subject to HMRC interpretation.

And when you get it wrong? You're looking at:

Back taxes on income you thought was tax-free

Interest on unpaid tax (currently running at 7.75% for late payment)

Penalties up to 100% of the unpaid tax if HMRC considers the error deliberate

Potential criminal prosecution in cases of serious fraud

The self-assessment system puts absolute responsibility on you to determine your status correctly. HMRC doesn't check your return before accepting it: they just assume you've got it right. Then, years later, they can open an enquiry using border data, bank records, and employment information to verify your declared residence status.

Most costly mistakes are entirely avoidable with proper professional advice upfront. Whether you're planning a move abroad, returning to the UK, or maintaining complex international arrangements, getting specialist input on the statutory residence test is one of the best investments you can make.

Getting Your SRT Status Right

The Statutory Residence Test isn't as simple as it first appears, and the cost of getting it wrong extends far beyond the immediate tax bill. Compliance failures can damage your relationship with HMRC, create disclosure obligations that complicate future tax years, and limit your options for international structuring.

At Global Tax Consulting, we specialise in UK residency planning for individuals with complex international arrangements. Our residency planning services include:

Detailed SRT analysis based on your specific circumstances

Day-count tracking and monitoring throughout the tax year

Split-year treatment eligibility assessment and claim preparation

Strategic planning to optimise your residence position before relocation

HMRC enquiry support if your residence status is challenged

If you're planning an international move, already living between countries, or simply want certainty about your UK residence status, we can help. The earlier you engage with specialist advice, the more options you'll have to structure your arrangements tax-efficiently.

Get in touch for a confidential, no-obligation quotation.

At Global Tax Consulting, we specialize in SRT assessments for expats, digital nomads, and internationally mobile professionals. Whether you're planning to leave the UK, you've already left, or you're a frequent traveler unsure of your status, we provide fixed-fee residency advice that gives you total clarity.

Left the UK but still earning from a UK employer, pension, or business? Discover how HMRC taxes non-residents and how to use tax treaties to your advantage.

Moving to the UK? Learn about the new FIG (Foreign Income and Gains) regime. Our beginner's guide explains how to get a 4-year tax holiday on foreign income.

Selling your UK home while living abroad? Learn how Capital Gains Tax (CGT) works for expats and how to report it correctly to HMRC. Get expert UK expat tax advice.

Master the UK Statutory Residence Test (SRT) for 2026. Learn how the automatic tests, sufficient ties, and the new FIG regime affect your expat tax status.

Missed reporting overseas earnings to HMRC? Learn how the Worldwide Disclosure Facility (WDF) works and how to fix your UK tax return without the stress.

HMRC’s Let Property Campaign: How to Declare Your Rental Income

Caught out with undeclared rental income? Our guide to HMRC's Let Property Campaign helps accidental landlords disclose tax safely and minimize penalties in 2026.

HMRC is using new 2026 CRS data rules to track e-money and offshore assets. Learn how voluntary disclosure can save you from 200% penalties and "nudge letters."

Selling property abroad? Compare DIY filing vs. hiring a UK tax advisor for your CGT return. Learn about HMRC's 60-day rule, currency traps, and expert tax advice for expats to avoid penalties.